3 Reasons PRPL is Risky and 1 Stock to Buy Instead

Purple has gotten torched over the last six months - since October 2024, its stock price has dropped 25.8% to $0.67 per share. This might have investors contemplating their next move.

Is now the time to buy Purple, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free .

Despite the more favorable entry price, we're swiping left on Purple for now. Here are three reasons why you should be careful with PRPL and a stock we'd rather own.

Why Do We Think Purple Will Underperform?

Founded by two brothers, Purple (NASDAQ:PRPL) creates sleep and home comfort products such as mattresses, pillows, and bedding accessories.

1. Long-Term Revenue Growth Disappoints

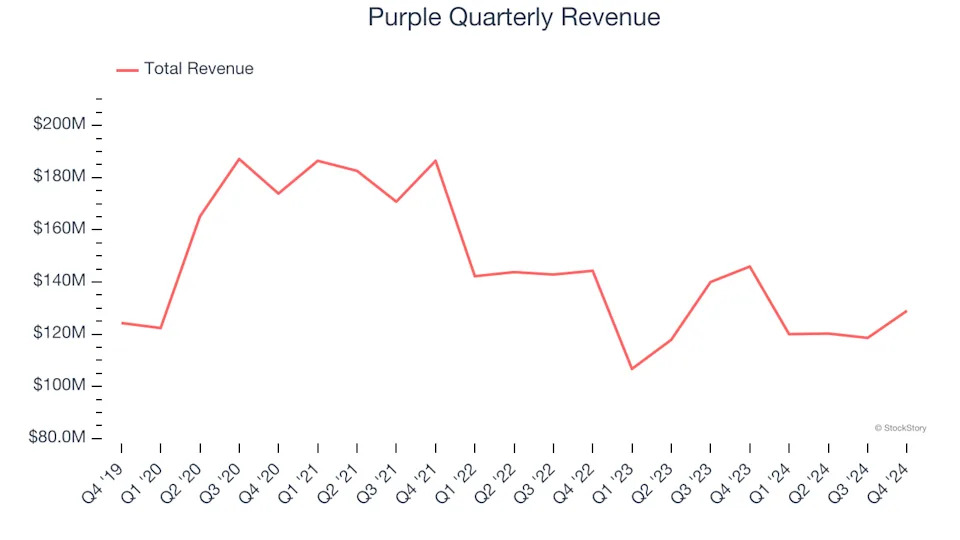

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Purple’s sales grew at a weak 2.6% compounded annual growth rate over the last five years. This fell short of our benchmarks.

2. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Purple’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

3. Short Cash Runway Exposes Shareholders to Potential Dilution

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Purple burned through $25.09 million of cash over the last year, and its $184.2 million of debt exceeds the $29.01 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Purple’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Purple until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.