3 Reasons to Avoid AGCO and 1 Stock to Buy Instead

Over the past six months, AGCO’s shares (currently trading at $80.94) have posted a disappointing 17.9% loss while the S&P 500 was down 11%. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy AGCO, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free .

Even with the cheaper entry price, we don't have much confidence in AGCO. Here are three reasons why we avoid AGCO and a stock we'd rather own.

Why Do We Think AGCO Will Underperform?

With a history that features both organic growth and acquisitions, AGCO (NYSE:AGCO) designs, manufactures, and sells agricultural machinery and related technology.

1. Core Business Falling Behind as Demand Declines

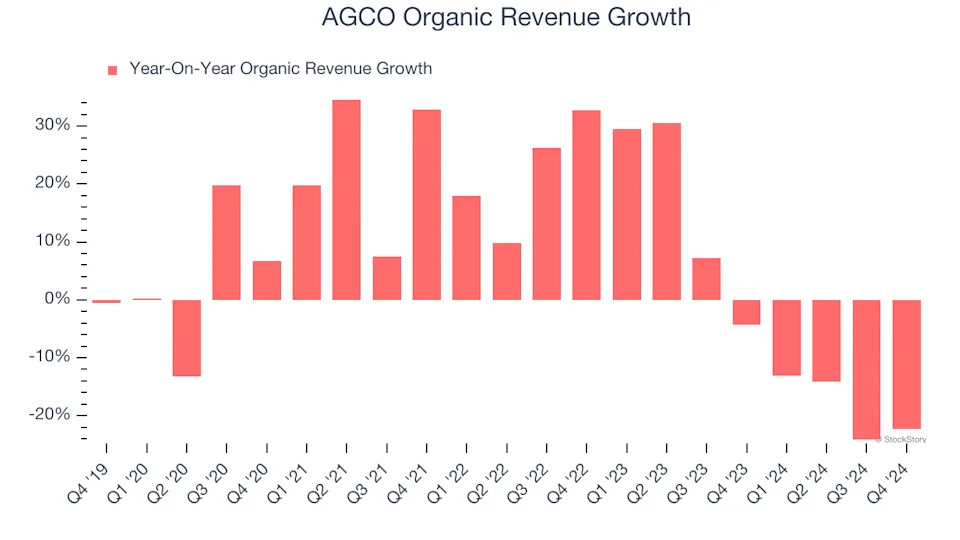

In addition to reported revenue, organic revenue is a useful data point for analyzing Agricultural Machinery companies. This metric gives visibility into AGCO’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, AGCO’s organic revenue averaged 1.3% year-on-year declines. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests AGCO might have to lean into acquisitions to grow, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

2. Shrinking Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Analyzing the trend in its profitability, AGCO’s operating margin decreased by 7.6 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. AGCO’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was negative 1%.

3. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.