3 Reasons to Avoid TPC and 1 Stock to Buy Instead

Tutor Perini has gotten torched over the last six months - since October 2024, its stock price has dropped 23.4% to $20.26 per share. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Tutor Perini, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free .

Even with the cheaper entry price, we're swiping left on Tutor Perini for now. Here are three reasons why we avoid TPC and a stock we'd rather own.

Why Do We Think Tutor Perini Will Underperform?

Known for constructing the Philadelphia Eagles’ Stadium, Tutor Perini (NYSE:TPC) is a civil and building construction company offering diversified general contracting and design-build services.

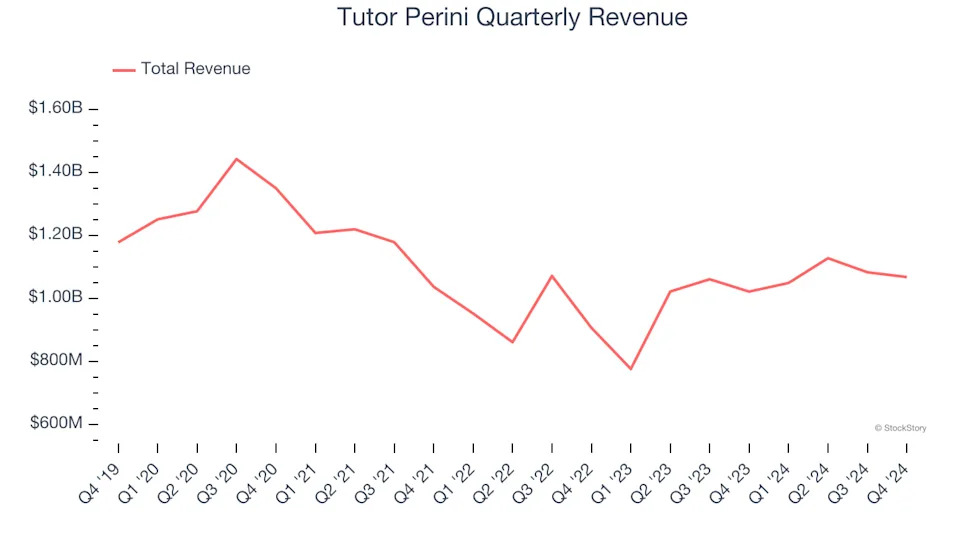

1. Long-Term Revenue Growth Flatter Than a Pancake

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Tutor Perini struggled to consistently increase demand as its $4.33 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and signals it’s a low quality business.

2. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Tutor Perini’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

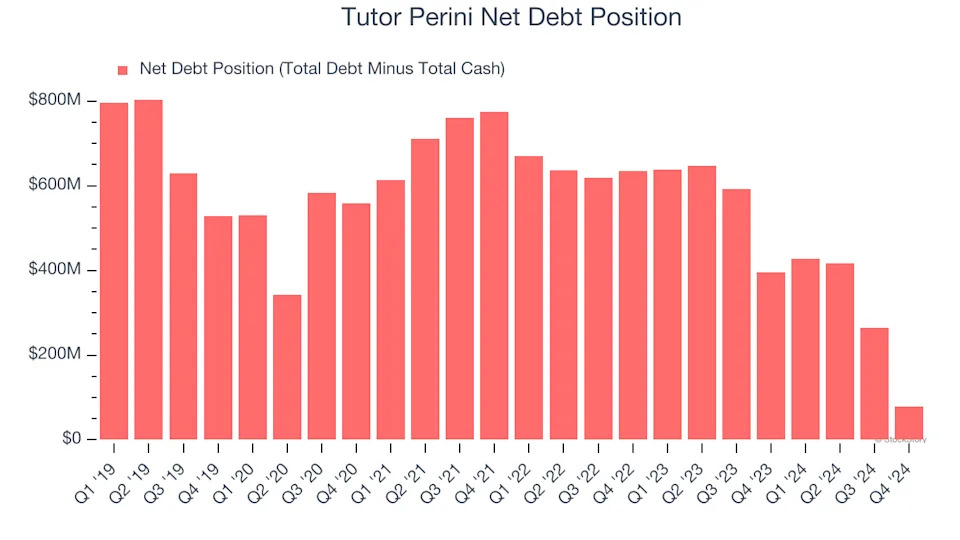

3. Restricted Access to Capital Increases Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Tutor Perini posted negative $12.12 million of EBITDA over the last 12 months, and its $534.1 million of debt exceeds the $455.1 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade Tutor Perini if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope Tutor Perini can improve its profitability and remain cautious until then.