3 Reasons to Sell TDC and 1 Stock to Buy Instead

Teradata has gotten torched over the last six months - since September 2024, its stock price has dropped 23.8% to $23.11 per share. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Teradata, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free .

Even with the cheaper entry price, we don't have much confidence in Teradata. Here are three reasons why TDC doesn't excite us and a stock we'd rather own.

Why Do We Think Teradata Will Underperform?

Part of point-of-sale and ATM company NCR from 1991 to 2007, Teradata (NYSE:TDC) offers a software-as-service platform that helps organizations manage and analyze their data across multiple storages.

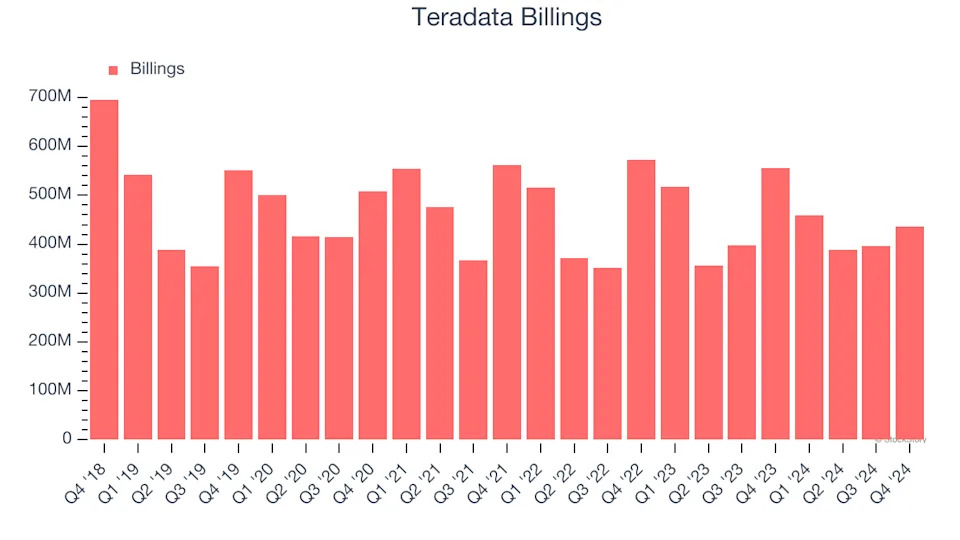

1. Declining Billings Reflect Product and Sales Weakness

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Teradata’s billings came in at $436 million in Q4, and it averaged 6.1% year-on-year declines over the last four quarters. This performance was underwhelming and shows the company faced challenges in acquiring and retaining customers. It also suggests there may be increasing competition or market saturation.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Teradata’s revenue to drop by 6.6%, a decrease from its 3% annualized declines for the past three years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

3. Low Gross Margin Reveals Weak Structural Profitability

For software companies like Teradata, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Teradata’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 60.6% gross margin over the last year. Said differently, Teradata had to pay a chunky $39.37 to its service providers for every $100 in revenue.