3 Reasons to Sell RPD and 1 Stock to Buy Instead

Over the past six months, Rapid7’s shares (currently trading at $29.56) have posted a disappointing 16.7% loss while the S&P 500 was flat. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Rapid7, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free .

Even with the cheaper entry price, we're swiping left on Rapid7 for now. Here are three reasons why you should be careful with RPD and a stock we'd rather own.

Why Is Rapid7 Not Exciting?

Founded in 2000 with the idea that network security comes before endpoint security, Rapid7 (NASDAQ:RPD) provides software as a service that helps companies understand where they are exposed to cyber security risks, quickly detect breaches and respond to them.

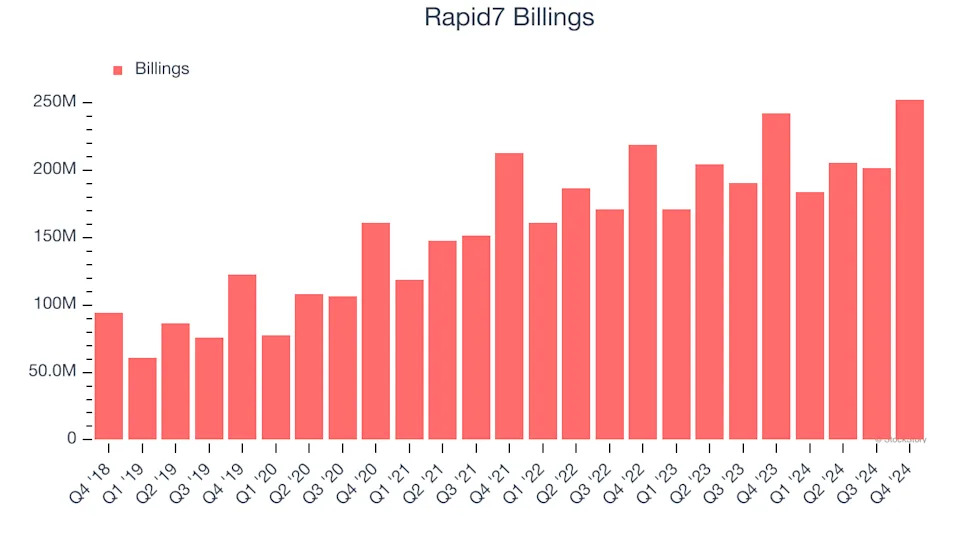

1. Weak Billings Point to Soft Demand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Rapid7’s billings came in at $252.6 million in Q4, and over the last four quarters, its year-on-year growth averaged 4.6%. This performance was underwhelming and suggests that increasing competition is causing challenges in acquiring/retaining customers.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Rapid7’s revenue to rise by 2.5%, a deceleration versus its 16.4% annualized growth for the past three years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

3. Long Payback Periods Delay Returns

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Rapid7’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between Rapid7’s products and its peers.