3 Reasons to Avoid VSEC and 1 Stock to Buy Instead

What a time it’s been for VSE Corporation. In the past six months alone, the company’s stock price has increased by a massive 44%, reaching $120 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy VSE Corporation, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free .

Despite the momentum, we don't have much confidence in VSE Corporation. Here are three reasons why you should be careful with VSEC and a stock we'd rather own.

Why Is VSE Corporation Not Exciting?

With roots dating back to 1959 and a strategic focus on extending the life of transportation assets, VSE Corporation (NASDAQ:VSEC) provides aftermarket parts distribution and maintenance, repair, and overhaul services for aircraft and vehicle fleets in commercial and government markets.

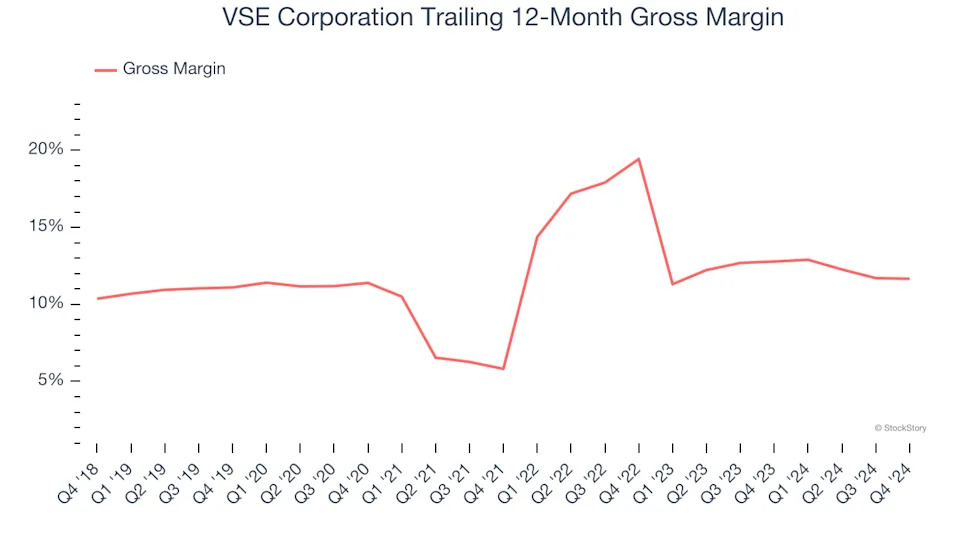

1. Low Gross Margin Reveals Weak Structural Profitability

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

VSE Corporation has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 12.2% gross margin over the last five years. Said differently, VSE Corporation had to pay a chunky $87.81 to its suppliers for every $100 in revenue.

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for VSE Corporation, its EPS declined by 2.3% annually over the last five years while its revenue grew by 7.5%. This tells us the company became less profitable on a per-share basis as it expanded.

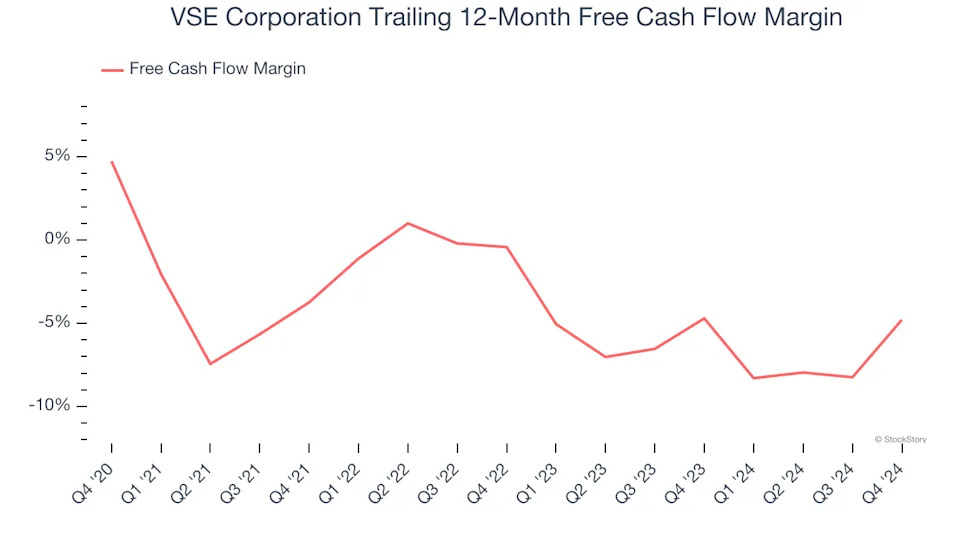

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, VSE Corporation’s margin dropped by 9.5 percentage points over the last five years. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s becoming a more capital-intensive business. VSE Corporation’s free cash flow margin for the trailing 12 months was negative 4.8%.