Q4 Rundown: Teradyne (NASDAQ:TER) Vs Other Semiconductor Manufacturing Stocks

Looking back on semiconductor manufacturing stocks’ Q4 earnings, we examine this quarter’s best and worst performers, including Teradyne (NASDAQ:TER) and its peers.

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers, and data storage. The need for technologies like artificial intelligence, 5G networks, and smart cars is also creating the next wave of growth for the industry. Keeping up with this dynamism requires new tools that can design, fabricate, and test chips at ever smaller sizes and more complex architectures, creating a dire need for semiconductor capital manufacturing equipment.

The 14 semiconductor manufacturing stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 1.6% while next quarter’s revenue guidance was 1.8% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 9.1% since the latest earnings results.

Teradyne (NASDAQ:TER)

Sporting most major chip manufacturers as its customers, Teradyne (NASDAQ:TER) is a US-based supplier of automated test equipment for semiconductors as well as other technologies and devices.

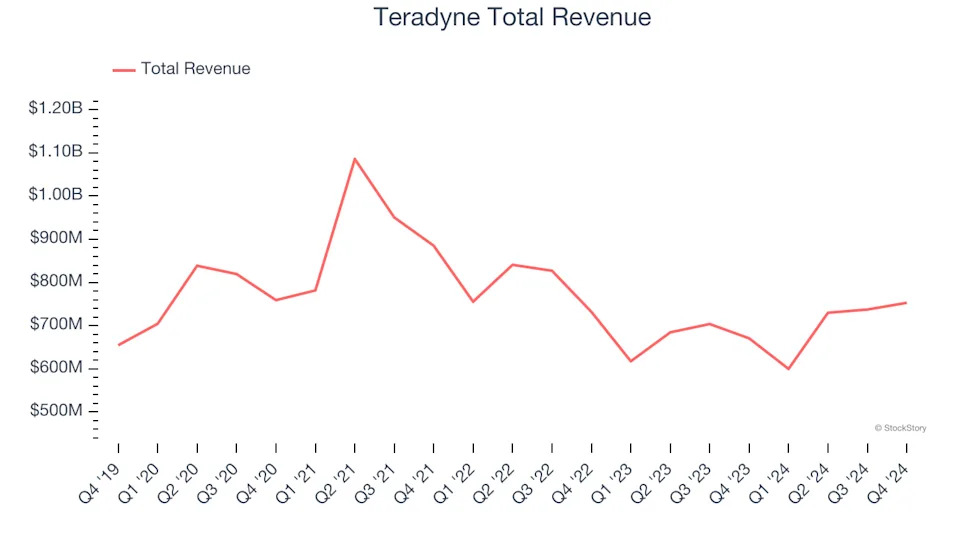

Teradyne reported revenues of $752.9 million, up 12.3% year on year. This print exceeded analysts’ expectations by 1.4%. Despite the top-line beat, it was still a mixed quarter for the company with a solid beat of analysts’ EPS estimates but a miss of analysts’ adjusted operating income estimates.

“Our Q4 results were toward the high end of our guidance range, driven by demand in our Semi Test business. For the quarter, AI compute and related memory remained strong while Mobile and Auto/Industrial exceeded our expectations,” said Teradyne CEO, Greg Smith.

The stock is down 26.5% since reporting and currently trades at $89.73.

Is now the time to buy Teradyne? Access our full analysis of the earnings results here, it’s free .

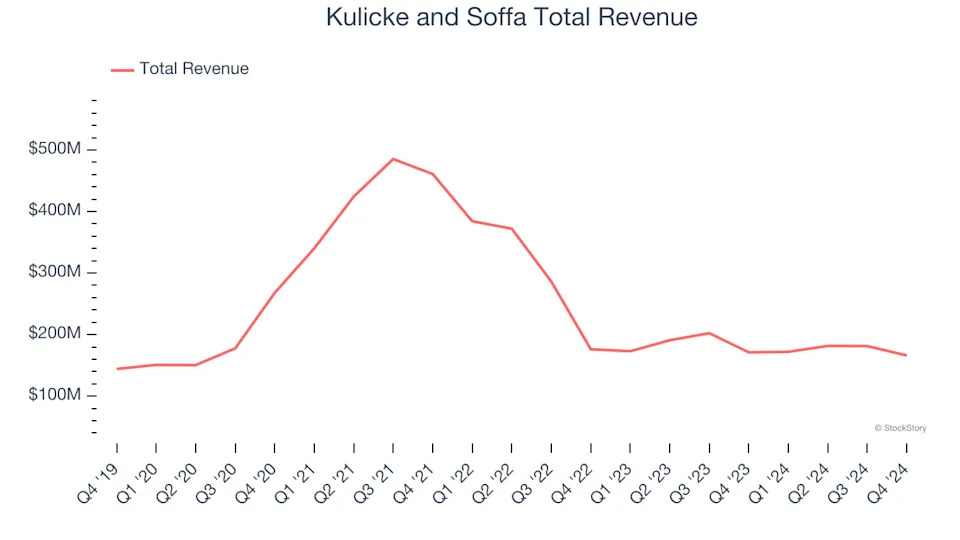

Best Q4: Kulicke and Soffa (NASDAQ:KLIC)

Headquartered in Singapore, Kulicke & Soffa (NASDAQ: KLIC) is a provider of production equipment and tools used to assemble semiconductor devices

Kulicke and Soffa reported revenues of $166.1 million, down 3% year on year, outperforming analysts’ expectations by 0.7%. The business had a very strong quarter with a significant improvement in its inventory levels and a solid beat of analysts’ EPS estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 16.8% since reporting. It currently trades at $36.13.

Is now the time to buy Kulicke and Soffa? Access our full analysis of the earnings results here, it’s free .