3 Reasons to Sell WAT and 1 Stock to Buy Instead

While the broader market has struggled with the S&P 500 down 1.7% since September 2024, Waters Corporation has surged ahead as its stock price has climbed by 13.1% to $382.94 per share. This run-up might have investors contemplating their next move.

Is now the time to buy Waters Corporation, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free .

We’re glad investors have benefited from the price increase, but we're swiping left on Waters Corporation for now. Here are three reasons why you should be careful with WAT and a stock we'd rather own.

Why Is Waters Corporation Not Exciting?

Founded in 1958 and pioneering innovations in laboratory analysis for over six decades, Waters (NYSE:WAT) develops and manufactures analytical instruments, software, and consumables for liquid chromatography, mass spectrometry, and thermal analysis used in scientific research and quality testing.

1. Core Business Falling Behind as Demand Declines

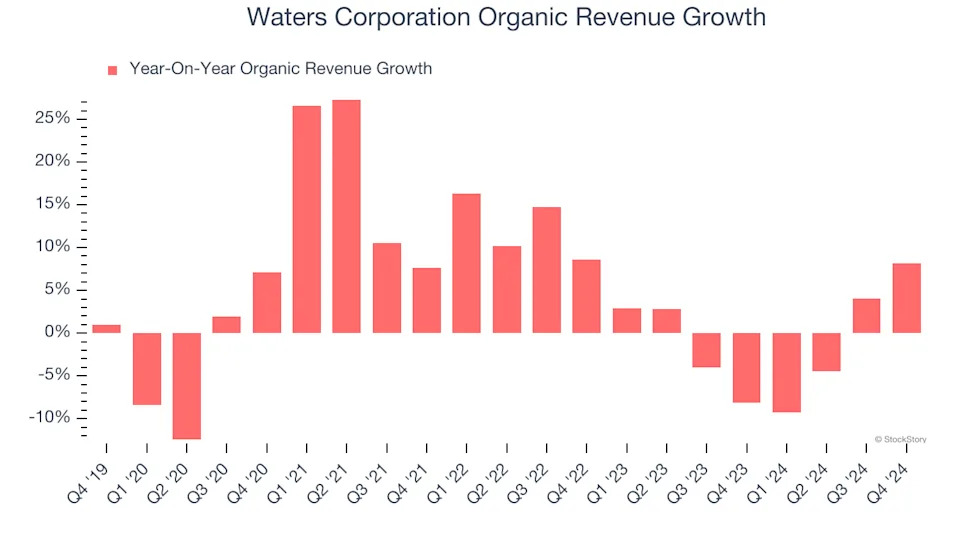

Investors interested in Research Tools & Consumables companies should track organic revenue in addition to reported revenue. This metric gives visibility into Waters Corporation’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Waters Corporation’s organic revenue averaged 1% year-on-year declines. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests Waters Corporation might have to lean into acquisitions to grow, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

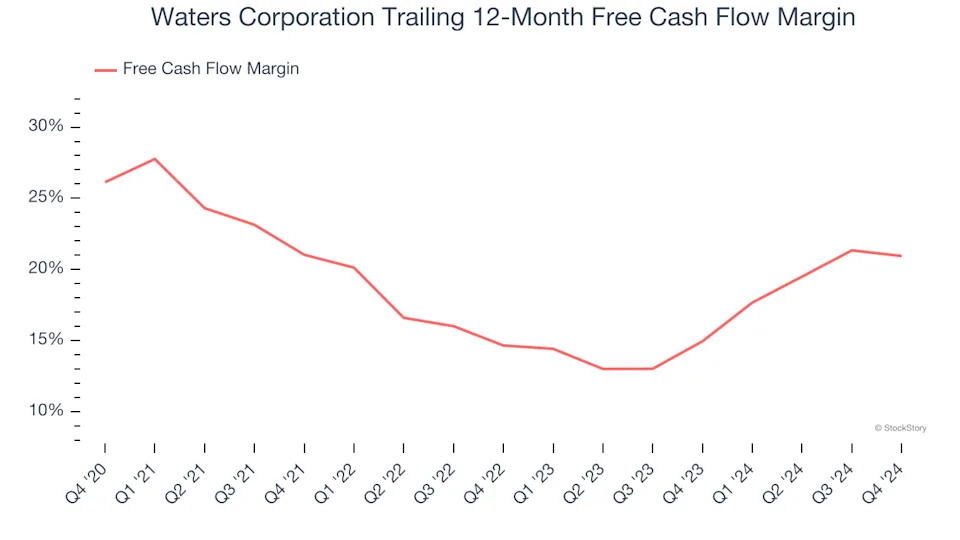

2. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Waters Corporation’s margin dropped by 5.2 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal increasing investment needs and capital intensity. Waters Corporation’s free cash flow margin for the trailing 12 months was 20.9%.

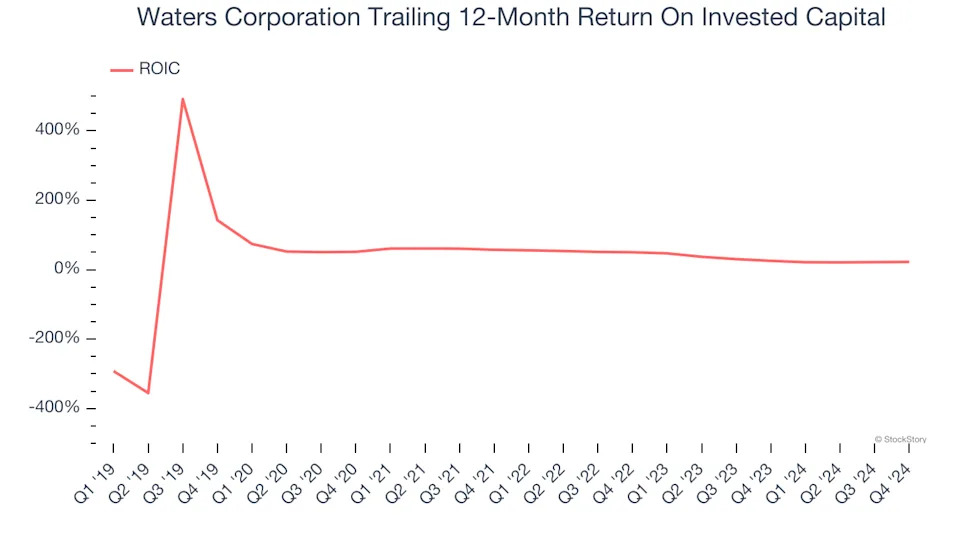

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).