3 Reasons to Avoid FLYW and 1 Stock to Buy Instead

Flywire’s stock price has taken a beating over the past six months, shedding 37.8% of its value and falling to $10.36 per share. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Flywire, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free .

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons why there are better opportunities than FLYW and a stock we'd rather own.

Why Is Flywire Not Exciting?

Originally created to process international tuition payments for universities, Flywire (NASDAQ:FLYW) is a cross border payments processor and software platform focusing on complex, high-value transactions like education, healthcare and B2B payments.

1. Low Gross Margin Reveals Weak Structural Profitability

For software companies like Flywire, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Flywire’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 63.7% gross margin over the last year. That means Flywire paid its providers a lot of money ($36.34 for every $100 in revenue) to run its business.

2. Long Payback Periods Delay Returns

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Flywire’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

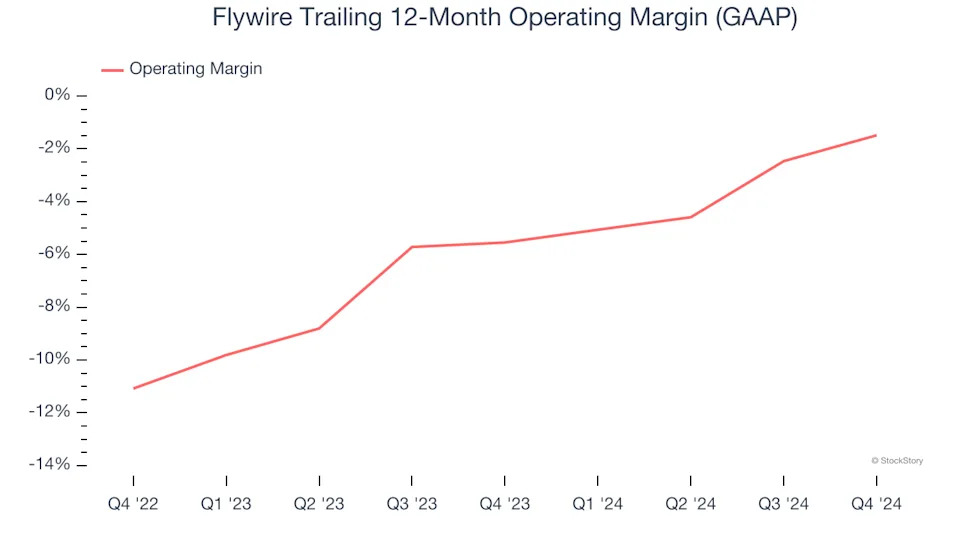

3. Operating Losses Sound the Alarms

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.