3 Reasons DRVN is Risky and 1 Stock to Buy Instead

Even during a down period for the markets, Driven Brands has gone against the grain, climbing to $16.60. Its shares have yielded a 17.4% return over the last six months, beating the S&P 500 by 18.4%. This performance may have investors wondering how to approach the situation.

Is now the time to buy Driven Brands, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free .

Despite the momentum, we're cautious about Driven Brands. Here are three reasons why we avoid DRVN and a stock we'd rather own.

Why Is Driven Brands Not Exciting?

With a diverse portfolio of well-known brands including CARSTAR, Maaco, Meineke, and Take 5 Oil Change, Driven Brands (NASDAQ:DRVN) operates North America's largest automotive services company with approximately 5,000 locations offering maintenance, car wash, paint, collision, and glass repair services.

1. Core Business Falling Behind as Demand Plateaus

We can better understand Industrial & Environmental Services companies by analyzing their organic revenue. This metric gives visibility into Driven Brands’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Driven Brands failed to grow its organic revenue. This performance slightly lagged the sector and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests Driven Brands might have to lean into acquisitions to accelerate growth, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

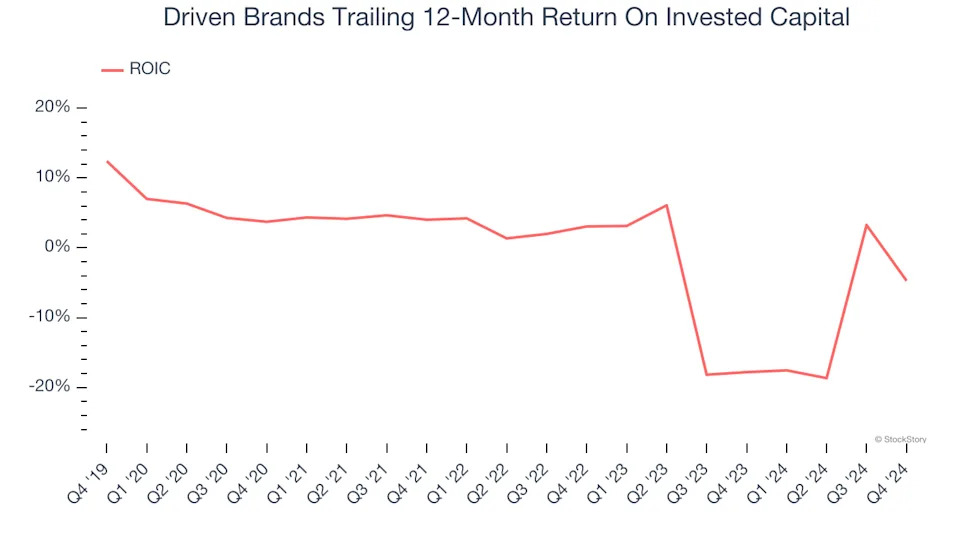

2. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Driven Brands’s ROIC has decreased significantly over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

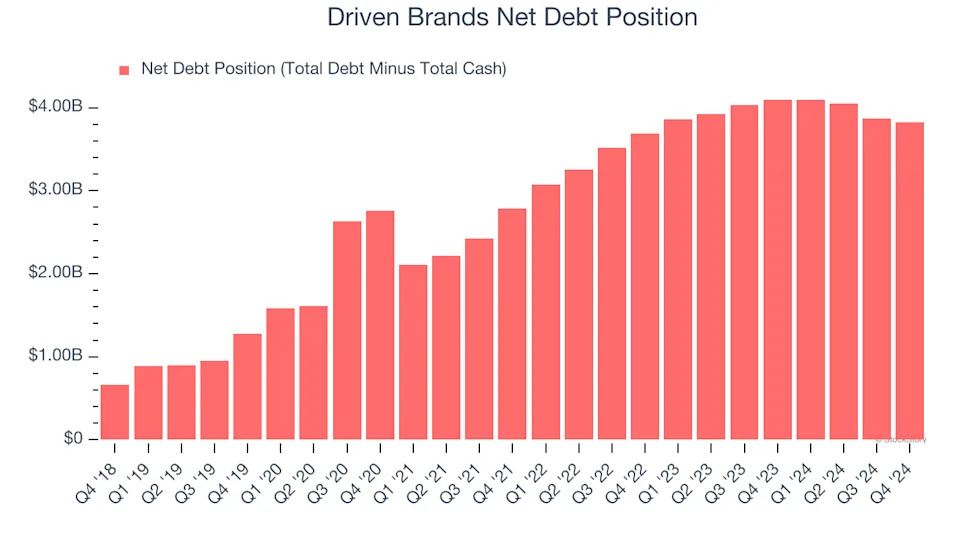

3. Short Cash Runway Exposes Shareholders to Potential Dilution

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.