Goldman just cut its US stock forecast. It lays out 3 things that could spark a recovery.

The near 10% correction in the S&P 500 over the past month is rattling investors, but Goldman Sachs says there's a pathway for a recovery.

David Kostin, chief US equity strategist at the bank, issued a note on Tuesday that included a reduction in the bank's year-end price target for the S&P 500 from 6,500 to 6,200.

Kostin blamed economic uncertainties related to the Trump administration's trade policy as the main reason for the decrease, arguing that earnings and valuation multiples will be pressured as long as the US continues down the tariff path.

"Our rule of thumb is that every 5 pp increase in the US tariff rate reduces S&P 500 EPS by roughly 1-2%, assuming companies are able to pass through most of the tariffs to consumers," Kostin said.

However, Kostin said three factors could drive a swift recovery in the stock market — and he added that only one of these things needs to be triggered for the rally to restart.

Change in the economic growth outlook

A growth scare has gripped Wall Street in recent weeks, with the Atlanta Fed's GDPNow growth forecast for first-quarter GDP growth plunging from nearly 4% in January to -2.4% last week.

Any reversal in economic growth expectations would spark a swift rally in equities, according to Kostin.

"We believe investors will require either a catalyst that improves the economic growth outlook or clear asymmetry to the upside before they try to 'catch the falling knife' and reverse the recent market momentum," Kostin said.

Improving economic data or a change in the Trump administration's tariff policy are candidates that could spark such a rally.

The stock market got a brief taste of this on Wednesday when a cooler-than-expected February CPI report sparked a 1% rally in the S&P 500.

Valuations have to hit attractive levels

Kostin wants to see stock market valuations price in economic growth that is "well below" the bank's baseline forecast.

That's starting to happen.

The S&P 500 is trading at a forward 12-month price-to-earnings ratio of 20.1x, which is slightly below Goldman's estimate for the multiple to be at 20.6x at the end of the year.

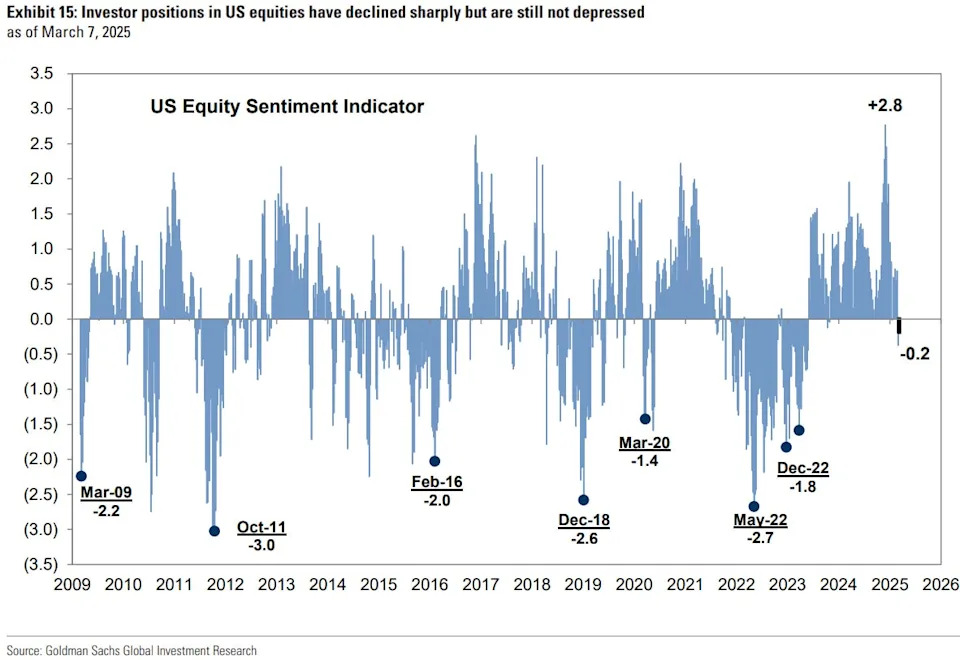

Meanwhile, the mega-cap tech stocks are trading at their lowest valuation premium to the rest of the S&P 500 components since 2017.